Australia’s property obsession faces the numbers as 20 years of returns, inflation impacts, taxes, and costs reveal how homes stack up against shares.

In Australia, people talk about property prices as often as they talk about the weather. It slips into convos at work and around the family barbeque

Owning property feels like the most pressing concern for everyone around you as soon as you hit 30 (or even earlier)! So it’s no surprise that owning property is known as the ‘Great Australian Dream’... but should it be?

Today, we want to look at the cold hard data to see if our property obsession stacks up from a financial perspective.

How has the Australian residential property market performed over the past 20 years compared to other forms of investing like shares? And what are the important factors to consider on both sides of the equation?

A lot has happened in the last 20 years including a global financial crisis (2008), the rise of FAANG stocks, a global pandemic and months in social lockdown! 😱

These events have no doubt impacted the property and share markets in unique ways.

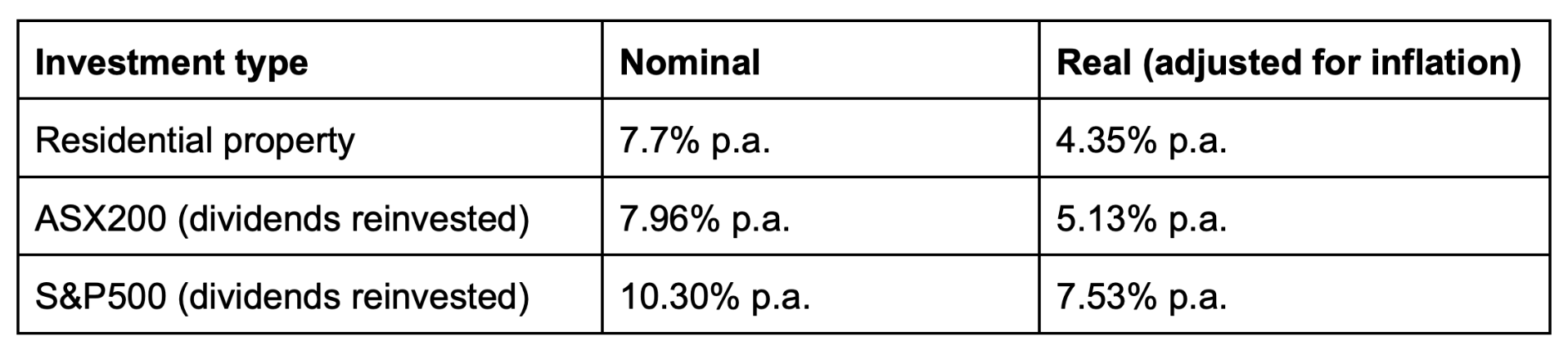

But the residential property market in Australia as stayed resilient throughout all these changes. In fact, the residential property market has delivered approximately 154% return between 2005 and 2024 - averaging out to around 7.7% of annual growth.

Meanwhile, the ASX200 returned a compound annual growth rate (CAGR) of 7.96% between 2005 and 2025 (if you reinvested all your dividends) and the S&P500 returned 10.30% over the same period.

Over the last 20 years, Australia has struggled with sky high inflation - cumulatively, equating to about 67% rise in prices. So when inflation is taken into account, it erodes a lot of the growth we see because our money has less purchasing power.

Below are the REAL return rates, after adjusting for inflation.

Now, you might be thinking shares are the better investment after this simple comparison, but hold your judgement until the end because there’s more to consider.

Tax is where property starts to shine. When Australians sell their assets at a profit on an investment (like an investment property or investments in the share market), they need to pay ‘capital gains tax’ (CGT).

Shares sold at a profit are subject to CGT. If the shares have been held for longer than 12 months, a 50% CGT discount may apply to reduce tax payable.

On the other hand, residential property that is considered your main residence is exempt from CGT. This means any capital growth you benefit from at the time of sale won’t be taxed at all for capital gains.

High expenses are the silent killer of growth… And anyone who owns a home can tell you - maintaining property ain’t cheap!

Below are common ongoing expenses that come with owning property:

Although an investment portfolio usually has less ongoing costs, it's still important to be mindful of the fees that come from trading shares and maintaining the portfolio.

Stay tuned for part 2 where we’ll look at an example scenario that incorporates all these factors … And finally figure out whether the Aussie property obsession is justified!

Disclaimer: Flux Technologies Pty Ltd (ABN 86 634 507 172) is an authorised representative (Representative No. 525288) of Mozo Pty Ltd who is the holder of AFSL No. 328141. We also provide general advice on credit products under our own Australian Credit Licence No. 530103. The product information presented does not constitute an offer and we are not recommending or suggesting any particular product. Any product advice presented is of a general nature only, and is not to be taken as any sort of advice as it has not taken into account your personal circumstances, objectives, financial situation or needs. Flux may not cover all products available to you. Check out our Credit Guide and Financial Services Guide for more information.

All information contained in the Flux app, www.flux.finance, www.joinflux.com, app.flux.finance and any podcast of Flux Media Pty Ltd (ABN 27 639 804 345) is for education and entertainment purposes only. It is not intended as a substitute for professional financial, legal or tax advice. Flux Media Pty Ltd is the owner of the registered trade mark, 'What the Flux'. While we do our best to provide accurate information on the podcast, we accept no responsibility for any inaccuracies that may be communicated.

Sign up for Flux and join 100,000 members of the Flux family