Australia’s property obsession faces the numbers as 20 years of returns, inflation impacts, taxes, and costs reveal how homes stack up against shares.

Owning property is often considered the 'Great Australian Dream’. As Darryl Kerrigan from The Castle says “It's not a house, it's a home. A man's home is his castle”

But how often have you stopped to evaluate the numbers behind Australia’s obsession with property? In this two part article series we look at the data to answer this question for you!

In part 1, we reviewed the 20 year historical returns of both residential Australian property and investing in the stock market, after adjusting for inflation.

Then we also considered the different tax treatments, and common expenses that come with owning property or holding an investment portfolio that can silently erode growth over time.

Now, let’s get into the nitty gritty and look at an example that takes into account these factors.

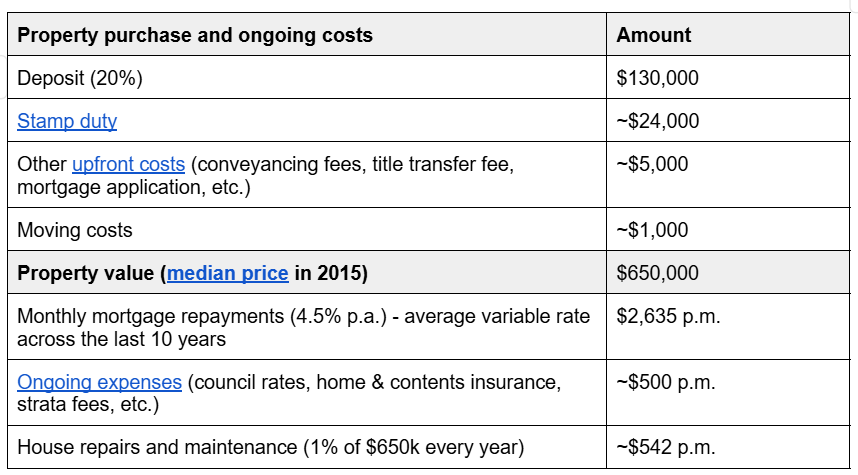

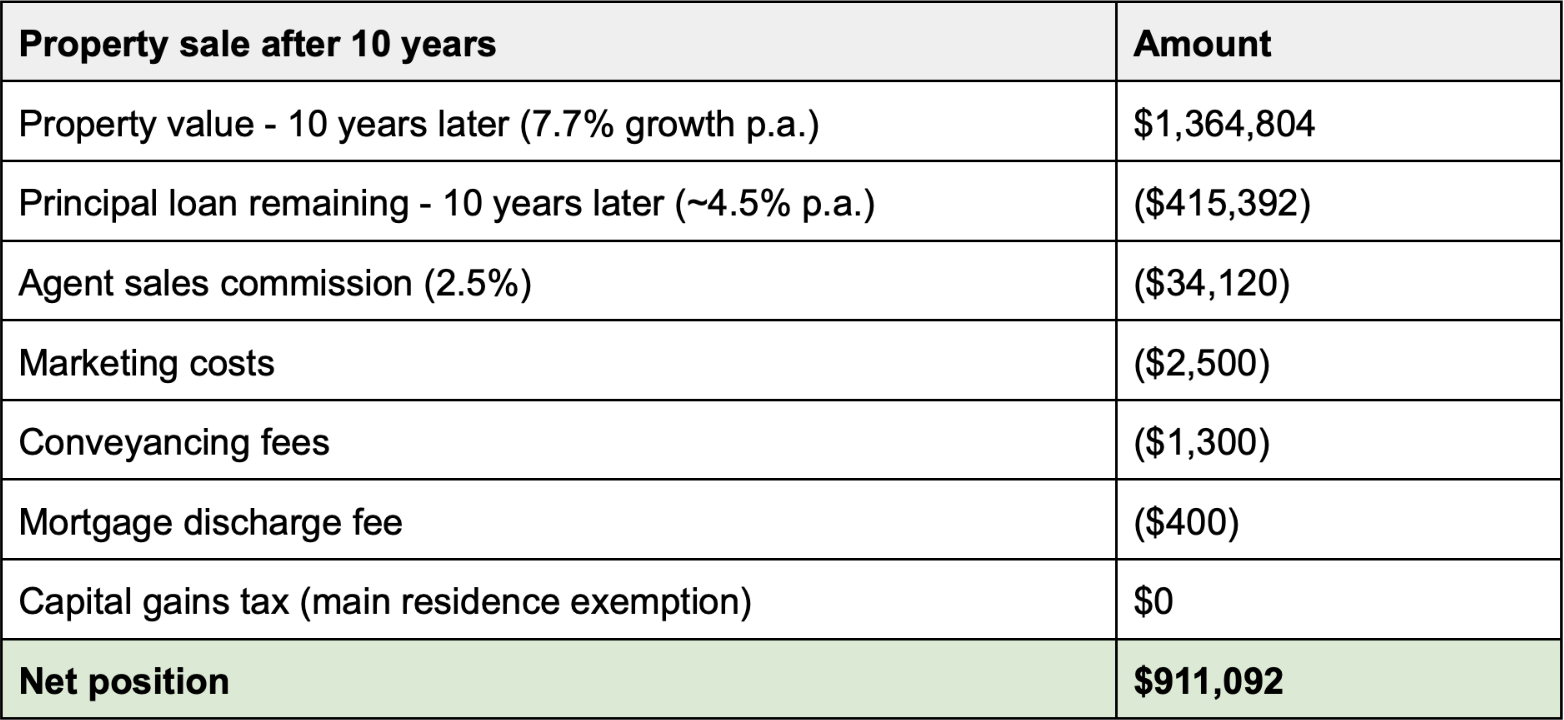

Rewind to 2015. Jess is renting which costs her $1,500 per month and she earns an annual salary of $120,000 plus super. Through disciplined saving she has $160,000 in cash that she can either use to buy a property with or invest into a share portfolio.

Scenario 1: Jess buys property in 2015 & sells after 10 years

Scenario 2: Jess invests in a share portfolio in 2015 & sells after 10 years

Sooo does this mean Aussies are right to be property obsessed afterall? …Maybe!

With property, you’re often starting off with a much larger initial investment (thanks to leverage!) which means compounding can work its magic at a faster rate.

But even after taking into account all the different factors that come with home ownership and investing in a share portfolio, this is a simplified version of real events.

In reality, past performance is not always an indication of future performance and the specific numbers for growth and expenses will be different based on the exact property that's purchased or the portfolio that's invested.

That’s why there’s another layer of considerations to think about in the property vs shares debate.

It’s not always about the money!

Now that we’ve evaluated the data and seen the numbers in action, here are several considerations which might carry a lot of non-monetary value.

Property pros:

Rent-vesting pros:

Whether you should follow the ‘great Australian dream’ somewhat boils down to your personal preferences, because at the end of the day there is no investment that doesn’t come without its risks!

But we hope these articles have helped shed some light on a worthy alternative to the ‘‘Great Australian Dream’. Even if you can’t (or don’t want to) buy property, there are other ways to grow your wealth over time!

Disclaimer: All information contained in the Flux app, www.flux.finance, www.joinflux.com, app.flux.finance and any podcast of Flux Media Pty Ltd (ABN 27 639 804 345) is for education and entertainment purposes only. It is not intended as a substitute for professional financial, legal or tax advice. While we do our best to provide accurate information on the podcast, we accept no responsibility for any inaccuracies that may be communicated.

Flux does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) and ASIC RG 36.66. Flux Technologies Pty Ltd provides general advice on credit products under our own Australian Credit Licence No. 530103.

Sign up for Flux and join 100,000 members of the Flux family