Super is often treated as something to “set-and-forget", but your investment choices can make a huge difference to your super balance!

In partnership with

Most people treat their super like the spare room at home. Stuff gets thrown in. The door closes. And you promise yourself you’ll sort it out “one day”.

And while the retiree version of you might feel like a stranger to you now, the decisions you make today will determine how well future-you can live.

Often super is treated as something to “set-and-forget”. The problem is decades of small decisions (or indecisions) are quietly stacking up in the background.

When you’re young and have time on your side, smart decisions can compound into significant growth. Put simply, the earlier you start caring about your superannuation the better!

Meet Bianca.

Bianca is starting her first job out of university and has not chosen a super fund or a super investment option. As a default, her employer opens a MySuper fund for her and contributes her money to the default MySuper investment option.

While there isn’t anything wrong with this approach, this one-size-fits-all investment strategy doesn’t reflect her age, risk tolerance or personal values.

But what happens if she makes one small change - like shifting her investment option?

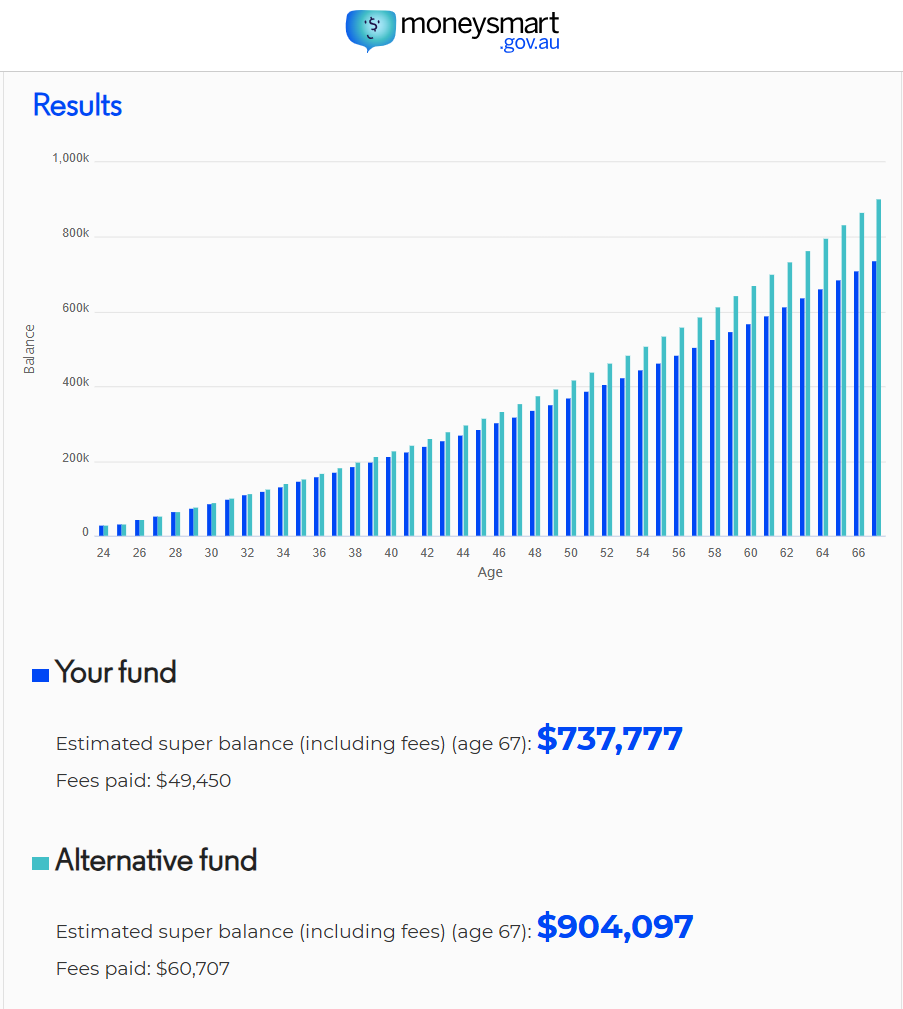

Assumptions: 25 years old, $95,000 salary, 12% p.a. super guarantee

MySuper investment (default): Balanced (6.2% p.a.) investment option

Alternative investment: High Growth (7% p.a.) investment option

In this example, the super fund returns 7% per annum (instead of 6.2%) and you can see that switching investment options has grown Bianca's super balance by over $167,000 by retirement at 67. More importantly, decisions like these give you the opportunity to tailor your investment strategy to your personal circumstances.

The average Australian retires with around $392,274 (female) to $448,518 (male) in their superannuation. And your super is one of the largest investments you’ll ever manage in life.

So how come it’s the asset you spend the least time understanding and reviewing?

By now you probably get it, having choices for your super matters A LOT. If you’re wondering what your options are, we got you bestie.

Check out our previous article on pooled vs direct investments, and if you haven’t already, learn the difference between industry, retail, and SMSF super structures too.

Netwealth Super Accelerator gives you greater choice and control over how your super is invested.

Designed for people who want to be more hands‑on, it allows you to invest in a way that reflects what matters to you, whether that’s your age, risk tolerance, financial goals, market views or personal values. It gives you access to a wide range of leading investment options, right at your fingertips.

And remember, not choosing is still a choice (just one made by someone else). You might think that sticking to the default option is the same as staying “neutral”, but actually you’re outsourcing one of your biggest financial decisions without checking if it suits you.

Flux disclaimer:

The Information contained in this article is general information. It does not constitute legal, tax, credit or financial advice and is not tailored to an individual’s circumstances. You should consider your own personal circumstances and seek advice from your professional advisers before making any decisions that may impact your financial situation.

Netwealth disclaimer:

Netwealth Superannuation Services Pty Ltd issues Netwealth Super Accelerator. Netwealth Investments Limited issues the Netwealth Wealth Accelerator Multi-Asset Portfolio Service. Information contained within this post is of general nature only. Consider whether the products are appropriate for you and seek advice where required. To help you decide, read the PDS or IDPS Guide and TMD available at netwealth - Super & Investment Solutions - Investors & Wealth Professionals.

Sign up for Flux and join 100,000 members of the Flux family