Here's a brief overview of novated leases - how they work, the benefits and downsides to using one.

When your car sounds like it’s beatboxing and your mechanic knows you by name, it might be time to retire the wheels that you learned to parallel park in.

But we get it, new cars ain’t cheap and not everyone has an extra $20-$90k lying in their bank account to purchase a car outright.

Typically, car loans are considered bad debt because the value of a new car often drops 10-15% in the first year of ownership, and up to 15% every year after. However, there are ways to make this a financially savvy(er) move.

A novated lease is a specific type of car loan that gets paid with your pre-tax salary. This means you can make a tax saving while paying off your car loan. However, these loan arrangements are structured a bit differently to your standard car loan so it’s important to know the ins and outs before committing to one.

Firstly, this loan is only available to employees who are earning a salary. Similar to how salary sacrificing works, your employer can subtract a set amount from your fortnightly/monthly pre-tax income to pay for your car instead. (Lower taxable income = reduced taxes. Woohoo!)

But in a novated lease agreement, the amount that comes out of your pay check isn’t just paying off the car loan, it also covers all the running expenses of owning a car like insurance, fuel, servicing and registration costs. This makes it great for people who like predictability and don’t want to worry about unexpected car expenses.

It’s important to know, novated leases have a mandated residual value payment (aka balloon payment) at the end which is a lump sum amount that needs to be paid in order for you to fully own the car when your loan period finishes. Meanwhile with a standard car loan, you can choose to have a balloon amount or not.

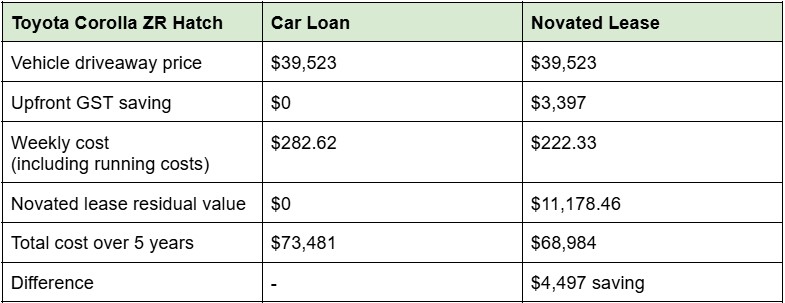

Here’s what it might look like to buy with a car loan vs novated lease:

This is a hypothetical example. Calculation assumes a driver in NSW, driving 15,000km per year, with an annual salary of $120,000. Running costs include fuel, comprehensive car insurance, registration, servicing, tyres, plus brokerage costs on the novated lease. Car finance assumes an interest rate of 7.24% and weekly repayments. Source: Money.com.au

💡 Tax savings - A novated lease is paid with pre-tax dollars. This means payments for your car will reduce your taxable income and provide a tax saving compared to a regular car loan.

💡 GST exemptions - You receive a GST exemption on the purchase of price of your vehicle plus any car running costs included in your novated lease. (However, the balloon payment at the end of your lease is subject to GST.)

💡 Extra benefits for EVs - Electric vehicles that are novated (up to the luxury car threshold of $91,387 in FY25/26) receive extra benefits like not being subject to fringe benefit tax - which is a special tax that’s usually applied to employee benefits.

🤔 Residual value payment - In order to fully own the car you need to pay a lump sum at the end of your lease term, known as a 'residual value payment' or 'balloon payment’. This can be a significant amount depending on the percentage of residual value left at the end of your loan.

🤔 Potential higher costs - Some employers have exclusive arrangements with specific novated lease providers, which reduces competition and your ability to secure the best deal. Some novated lease companies may also try to upsell extras that customers don’t really need, which can also bump up costs.

🤔 Loans can be ‘de-novated’ - The lease agreement is tied to you, not the employer. If you leave your job, the car will be ‘de-novated’ and you will be required to pay for it with your after-tax salary until you are employed and paid a salary again. Plus, not all workplaces offer novated leasing… so make sure you speak with your employer first to see if they are partnered with a novated lease provider.

While considering your options for buying a new (or used) car, it’s good to know your options and how you could potentially gain some tax perks with a novated lease. But the magic is in the maths, so it’s important to consult an accountant to ensure a novated lease makes sense for your personal situation.

Disclaimer: All information contained in the Flux app, www.flux.finance, www.joinflux.com, app.flux.finance and any podcast of Flux Media Pty Ltd (ABN 27 639 804 345) is for education and entertainment purposes only. It is not intended as a substitute for professional financial, legal or tax advice. While we do our best to provide accurate information on the podcast, we accept no responsibility for any inaccuracies that may be communicated.

Flux does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) and ASIC RG 36.66. Flux Technologies Pty Ltd provides general advice on credit products under our own Australian Credit Licence No. 530103.

Sign up for Flux and join 100,000 members of the Flux family