We're in tax season baby! Time to bust out those calculators and maximise those deductions.

We’re getting to that frosty time of year where our cars are iced over, the Kathmandu’s are out and tax time is looming.

Dun Dun Dunnnnnnnnnn!!!

Each year, we surrender a share of our hard-earned cash to the one and only Australian Tax Office, aka ATO.

Our tax is the price we pay for the benefits we get living in Australia.

Benefits like health, education, defence, public transport, and social security payments, also known as Centrelink.

And these taxes come in a range of flavours where you’ve got income tax, capital gains tax, property tax, goods and services tax, and so so many more.

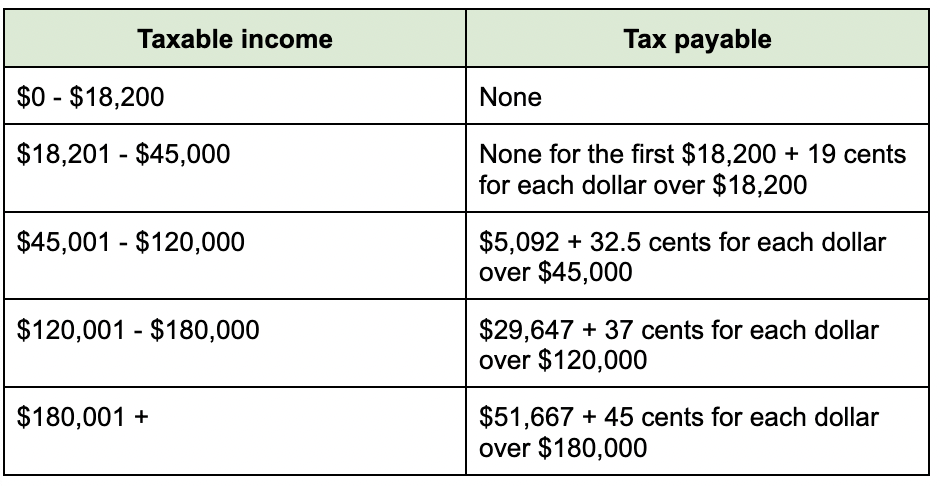

How does tax work in Australia?

Australia has a ‘progressive’ tax system.

Think of a progressive tax system like a video game, where the more you level up, the harder the quests become.

In the same way, the more you earn, the higher you go. And the higher you go, the higher percentage of tax you pay.

Your tax rate will go up as your taxable income increases.

And tax rates are broken up into tax brackets.

For the upcoming financial year, this is what they look like.

So if you’ve got taxable income of let’s say $75,000 and no deductions, then you’ll pay:

Your effective tax rate is usually lower than the rate of the tax bracket you're in because you're not paying all your tax at the highest rate that applies to you.

Australia’s tax system is also ‘self-assessable’, meaning we’re responsible for reporting our own taxable income to the ATO after 30th June each year.

It’s a bit like when your primary school teacher asked you to mark your own spelling tests.

Except this time, you can’t secretly change the answers while you’re marking to give yourself a higher score.

If you’ve overpaid your taxes, you’ll get a tax refund, and if you’ve underpaid, you’ll need to cough up some extra cash for the ATO.

What’s taxable income?

Taxable income = Assessable income - tax deductions.

Assessable income is ALL of the income earned for the year.

Think: your salary, your side-hustle cash from moonlighting as a DJ, capital gains, investment income, investments, pensions, and most government payments.

And your deductions are expenses that reduce your taxable income.

Oooh talk deductions to me:

It may not sound like it, but grinding through the boring math during tax-time can seriously pay off.

Deductions are expenses that can reduce your assessable income. And it could be a lot more than you think.

Research shows that 3.3 million self-lodging Aussies could be missing out on $300 million in unclaimed tax - that’s about $237.44 each.

And while tax can be a little tricky at first, like trying to learn a new card game, it can pay off massively for your finances.

Let’s be real, who doesn’t want to know how to maximise their deductions and reduce their tax obligation (legally of course)!

Head over to this month’s Flux Academy where we break down the whole 101 on all things tax with examples, analogies and really simple steps to help you with your tax.

Grab a glass of wine, beer, tea or milk (if you’re a weirdo) and give yourself an evening to sit and learn about your tax sitch.

Or jump in now to the tax topic you want to know about most:

Sign up for Flux and join 100,000 members of the Flux family