If you're a young Aussie dreaming of owning your first home, the stars might just be aligning thanks to two key changes

If you're a young Aussie dreaming of owning your first home, the stars might just be aligning.

On one side, we’ve got the Reserve Bank of Australia, who’s just cut the cash rate to 3.85%. That basically means it’s now cheaper to borrow money for a home loan.

On the other, we’ve got Albo and his government-backed 5% deposit scheme, kicking off from 1 Jan 2026.

Usually, you need to cough up a 20% property deposit if you want to get a loan from a bank. For instance, on an $820,000 home (the national median price), you’ll need a $164,000 deposit to get the banks comfortable.

But under this new scheme, you’ll only need 5% to get in the door. The government will guarantee the other 15%.

So instead of needing to save $164,000 on the $820,000 home, you’d only be required to front up a $41,000 deposit instead. Of course, you still need to be able to repay your mortgage repayments - but it’s suitable for first-home buyers who are struggling to save up a 20% deposit.

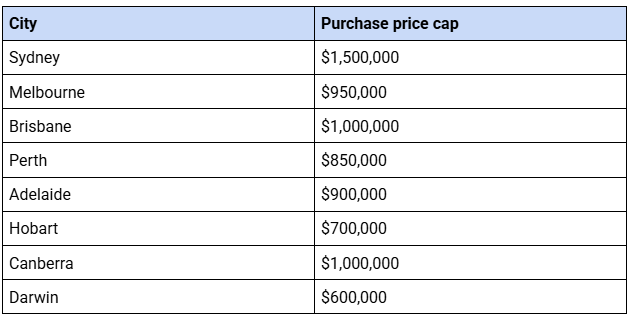

While the government's 5% deposit scheme is a game-changer for many first-home buyers, the scheme only applies to properties under certain price caps, which vary depending on where you're buying.

Historically, when interest rates drop, house prices go up. It’s kind of like clockwork — we've seen it in the 80s, 90s, and 2000s. Cheaper borrowing means more buyers in the market, and more buyers = more competition.

In fact, historical data shows that a 1% rate cut has led to an average 19% increase in house prices, particularly in premium markets across Melbourne and Sydney

Now throw in the new 5% deposit scheme starting in 2026, and you've got a recipe for even more demand. Property expert Louis Christopher reckons prices could jump 8% to 15% nationally in the year after it kicks in.

While a interest rate drop already stimulates housing prices, the 5% deposit scheme will likely put rocket fuel on the fire for houses below the price cap in each state.

The government's trying. They’ve pledged $10 billion to build 100,000 new homes just for first home buyers. Sounds great, right?

The catch? It’ll take eight years to roll out. That’s only about 8,500 homes a year — not exactly a flood of new supply.

And while they’re laying bricks, demand could go wild. More buyers + not enough homes = prices keep climbing.

We’re not saying you need to rush out and buy a house tomorrow. But if buying your first home is on the vision board, now’s a smart time to start getting your ducks in a row. A lower cash rate and a 5% deposit scheme don’t come around every day.

Disclaimer: All information contained in the Flux app, www.flux.finance, www.joinflux.com, app.flux.finance and any podcast of Flux Media Pty Ltd (ABN 27 639 804 345) is for education and entertainment purposes only. It is not intended as a substitute for professional financial, legal or tax advice. While we do our best to provide accurate information on the podcast, we accept no responsibility for any inaccuracies that may be communicated.

Flux does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) and ASIC RG 36.66. Flux Technologies Pty Ltd provides general advice on credit products under our own Australian Credit Licence No. 530103.

Sign up for Flux and join 100,000 members of the Flux family