The RBA keeps the cash rate steady at 3.6%, holding its ground as inflation rises again.

It’s that time of year again, when the board members of the Reserve Bank of Australia (RBA) come together to vote on the fate of Australia’s cash rate.

For those that have been following recent economic news, you might not be that surprised by the RBA’s decision to hold the cash rate at 3.60% this month.

Last week, the Australian Bureau of Statistics (ABS) released the latest quarterly inflation update. The annual Consumer Price Index (CPI) rate for the quarter ending September 2025 jumped to 3.2% (up from 2.1% in the June 2025 quarter) and “trimmed mean”, the RBA’s preferred measure of inflation, also saw an increase from 2.7% to 3.0%.

These numbers were higher than the RBA expected, which means consumer spending is rebounding faster and larger than anticipated. After the latest inflation numbers came out, the four major banks scrapped any predictions for further cuts this calendar year.

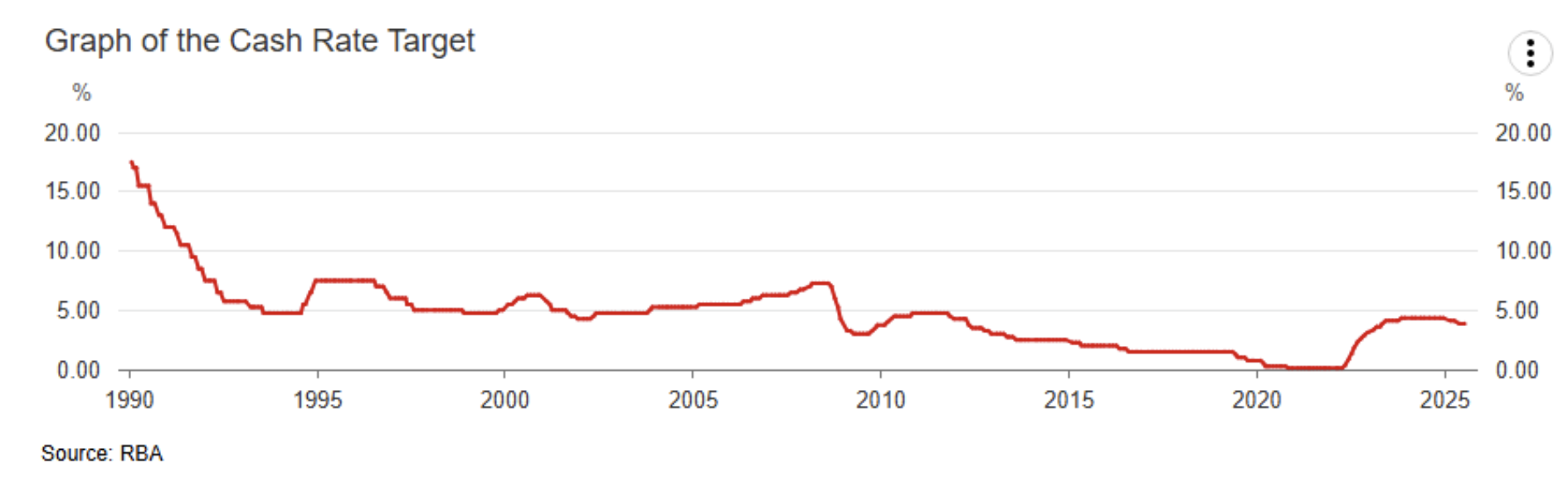

Back in May 2021, interest rates were at a historic low of 0.1% and economic conditions in Australia were pretty stable…except we started to see the signs of a dragon starting to rear its ugly ugly head.

Yep, with an economic slowdown coming out of the pandemic, and geo-political tensions globally, the inflation-dragon skyrocketed. In fact, by December 2022, the inflation-dragon had roared up to 7.8%. This meant prices for everyday goods like food, fuel and rent shot up.

To bring things back under control, the RBA went hardcore with thirteen cash rate increases in twenty two months…which eventually did its job of slowing down inflation.

The most recent quarterly “trimmed mean” figure is 3.0% (September, 2025), just within the RBA’s target range of 2-3%.

That’s why the slow but sure cutting cycle that started earlier this year is where the cash rate is being reduced to help stimulate the economy again.

But it’s all about finding that sweet spot: keeping the inflation dragon in check without dragging down economic growth.

We continue with the status quo.

If you’ve got a variable-rate home loan, your interest rate and mortgage repayments remain the same.

And good news for savers, your interest earning accounts just avoided a hit, so you’ll keep earning at your current interest rate.

While it might feel like the cash rate is currently quite high, you might have just gotten used to the rock-bottom cash rate during the pandemic.

In the bigger picture, it’s not all that extreme. Back in the mid-2000s, the cash rate was hanging around 6% to 7%, so today’s level is more middle-of-the-road.

Disclaimer: All information contained in the Flux app, www.flux.finance, www.joinflux.com, app.flux.finance and any podcast of Flux Media Pty Ltd (ABN 27 639 804 345) is for education and entertainment purposes only. It is not intended as a substitute for professional financial, legal or tax advice. While we do our best to provide accurate information on the podcast, we accept no responsibility for any inaccuracies that may be communicated.

Flux does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) and ASIC RG 36.66. Flux Technologies Pty Ltd provides general advice on credit products under our own Australian Credit Licence No. 530103.

Sign up for Flux and join 100,000 members of the Flux family