Capital gains tax just got its first major makeover since 1999, and it's about to shake up the housing market.

Reboots are everywhere right now.

Devil Wears Prada, Scrubs, Malcolm in the Middle, Legally Blonde... all the late 90s/early 2000s cult classics are back on our screens (but with weird Netflix lighting and shameless product placement).

Our government is clearly feeling nostalgic too. And Albo's big reboot? Straight outta 1999.

Capital Gains Tax (CGT) just got its first major makeover since then. So if you rent, own property, or one day hope to... you really should pay attention.

CGT is the tax you pay on profits from the sale of an asset, like shares, crypto, an investment property or even valuable collectables.

Here's a simple example. Say you buy an investment property for $700,000. Two years later you sell it for $800,000, meaning you've made a capital gain of $100,000.

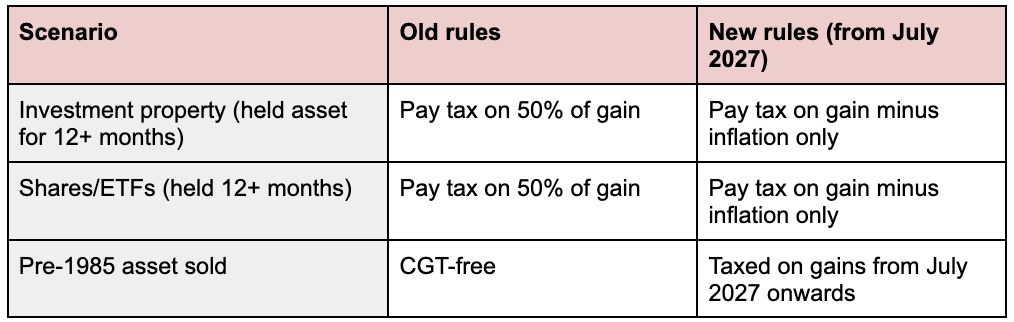

Since you held the property for over 12 months, you were entitled to a 50% CGT discount. The ATO created this rule to reward long-term investment. So you'd only pay tax on $50,000 of that gain, not the full $100,000.

If your salary is $80,000, you'd be taxed on a combined income of $130,000 ($80k salary + $50k capital gain) at your marginal rate. Not bad. But that's all about to change.

The government has scrapped the 50% CGT discount entirely and replaced it with an inflation indexation model.

Instead of automatically halving your taxable gain, you'll now only pay tax on your "real" profit, meaning the gain above inflation. So if your asset grew in value but a chunk of that growth was just keeping pace with rising prices, you won't be taxed on that part.

Here's how that plays out with the same example. Say inflation averaged 3% per year over the two years you held that investment property. On a $700,000 purchase, that's roughly $42,000 in inflation. So instead of paying tax on $50,000 (under the old 50% discount), you'd now pay tax on $58,000 (the $100,000 gain minus the $42,000 inflation adjustment).

Same capital gain, same profit, bigger tax bill. And the stronger the market, the bigger the gap.

On top of that, there's now a minimum 30% tax rate on capital gains. This isn't a new discount

The changes only apply to gains that arise after 1 July 2027, not the full gain on the asset. So if you bought an investment property years ago and sell it after that date, the new scheme will only apply to gains made on that asset from 1 July 2027. Everything before that is still under the old rules.

Yep! Cars and motorcycles are exempt because they're generally depreciating assets. Your main residential property is also in the clear. CGT could apply though if you use your home to generate income, like renting out a room or running a business from it.

CGT has been at the centre of debate for a long time. Some people think the current system is pretty unfair, benefiting those who have had property handed down generationally and locking out the rest. Think: the generation who bought property when it was actually affordable, versus the generation being told they'd manage it if they just cut back on the matcha.

Last year, millennial and Gen Z voters outnumbered baby boomers in every state and territory for the federal election. The Albanese government knows demographics are on its side. So it's coming for housing policy.

You'll probably fall into one of these camps:

Renters: The changes won't hit you directly. But economists warn that winding back the CGT discount could slow new rental property construction at a time when migration is pushing demand up. Rents could nudge higher, though because of existing lease agreements, any impact is likely 6 to 12 months away.

Property owner (your own home): If you own the property you live in and decide to sell, you're already exempt from CGT. These changes won't affect you.

Investment property owners: If you sell an investment property after 1 July 2027, you'll pay tax on a larger portion of your gain. Same profit, bigger tax bill.

Future investors: More tax on gains might make property investing a bit less attractive going forward. Worth factoring into any plans you're making now.

So, which category do you fall under, and what do you think of the changes?

All information contained in the Flux app, www.flux.finance, www.joinflux.com, app.flux.finance and any podcast of Flux Media Pty Ltd (ABN 27 639 804 345) is for education and entertainment purposes only. It is not intended as a substitute for professional financial, legal or tax advice. While we do our best to provide accurate information on the podcast, we accept no responsibility for any inaccuracies that may be communicated.

Flux does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) and ASIC RG 36.66. Flux Technologies Pty Ltd provides general advice on credit products under our own Australian Credit Licence No. 530103. The product information presented does not constitute an offer and we are not recommending or suggesting any particular product.

Sign up for Flux and join 100,000 members of the Flux family