Stagflation is one of the toughest investing environments, but history shows the right strategy can still uncover opportunities.

In partnership with:

If your group chat has gone from “should we book a trip?” to “I paid $7 for berries and my landlord is hiking up rent” you might not be the only ones.

Right now, Australians are being dealt a tough hand.

Inflation has been creeping up (making everyday essentials like rent, groceries, and bills, more expensive) and at the same time, the economy is slowing down.

In fact, there’s a name for this uncomfy situation we’re in and it’s called ✨stagflation✨

Stagflation is when economic growth slows down while prices keep rising.

Normally, inflation shows up when the economy is booming but stagflation flips that on its head - things get more expensive, but wages, jobs, and growth remain the same… or even slow down.

And that’s not all. On average, stagflation is the worst kind of environment for the stock market.

Yup, it’s not a vibe.

When the economy slows down, people start to feel the financial pinch pretty quickly. That usually means cutting back on spending, which then feeds back into weaker economic growth.

At the same time, businesses are dealing with rising costs. In a strong economy, they can usually pass those costs on to customers without too much drama. But when demand is already weak, that gets a lot harder so profit margins take the hit instead.

And this is the classic stagflation cycle - people spend less because times are tough, businesses earn less because people spend less, and the economy struggles to get back on its feet.

Short answer: not necessarily.

Historically, stock market returns during stagflation have been weaker but not disastrous.

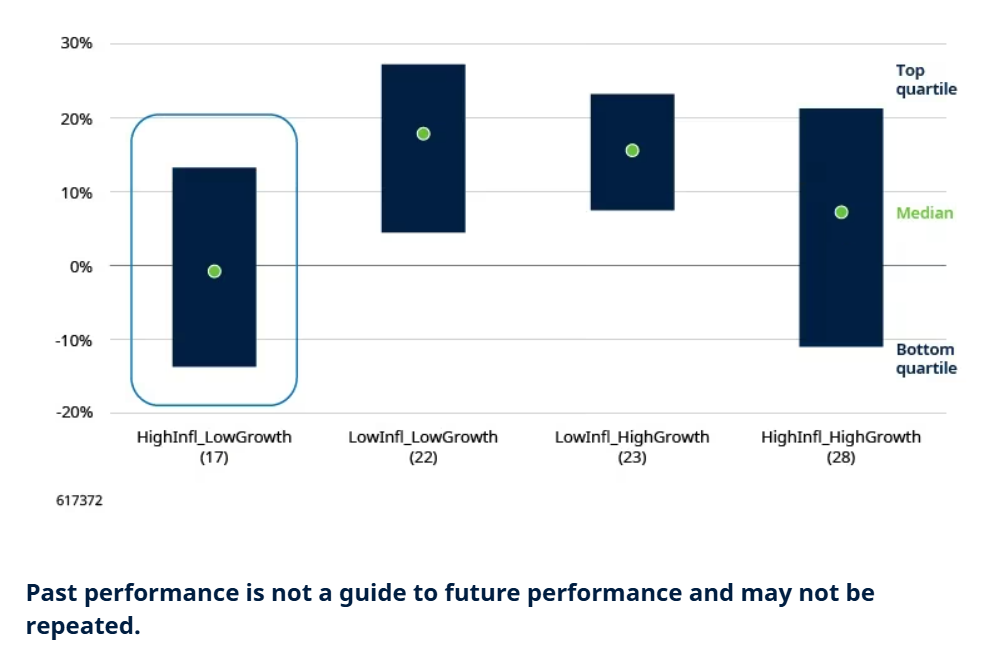

Graph: US stock market returns in years when inflation and economic growth are above or below their 10-year averages (1926–2025)

As expected, stocks tend to have a tougher time during stagflation compared with other economic environments, but it’s not all bad.

Since 1926, the median real return for equities during stagflation years is roughly 0%.

That’s lower than the long-term expectation for stocks, but it also means investors were, on average, at least keeping up with inflation.

The data also shows:

While it might be tempting to move into cash to avoid the volatility, cash might not be the safe haven investors believe.

When inflation is high, cash quietly loses value. That’s why, stocks have historically outperformed cash more often than not during stagflation periods.

This takes us back to a core investment principle: diversification.

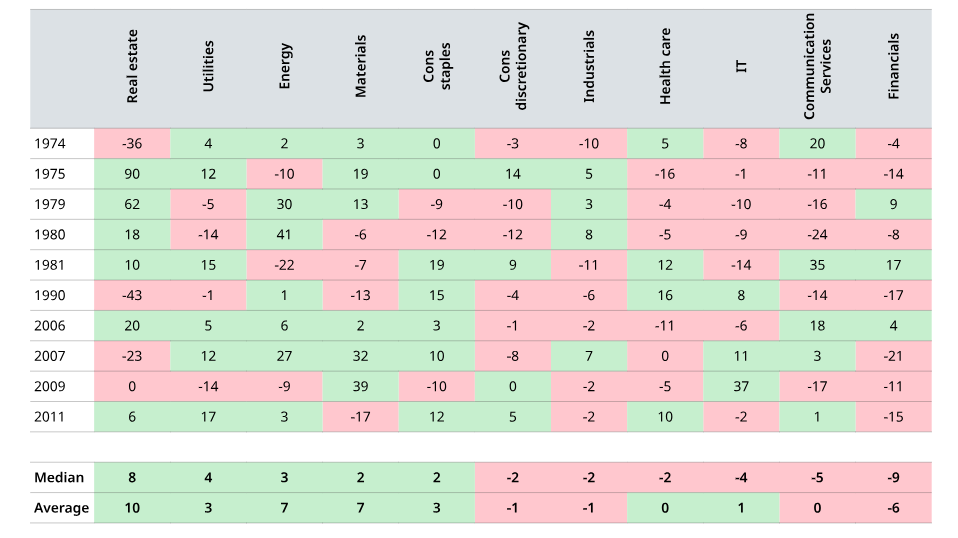

Data shows that some sectors do better than others during stagflation periods.

Graph 2: US sector returns during stagflation years (1974–2025)

Sectors that tend to perform better:

Sectors that tend to struggle:

In normal market conditions, broad market exposure (like passive index investing) can do a lot of the heavy lifting.

But stagflation is different. Instead of markets moving together, returns tend to spread out more across sectors and individual companies.

In this kind of environment, active strategies have potential to add value since managers have more opportunities to overweight resilient businesses (like defensive sectors or companies with pricing power) and underweight those more exposed to rising costs and weak demand.

Schroder Global Equity Alpha Fund is designed to navigate economic cycles as they unfold, identifying companies that are benefiting from these shifts rather than being disrupted by them.

All information contained in the Flux app, www.flux.finance, www.joinflux.com, app.flux.finance and any podcast of Flux Media Pty Ltd (ABN 27 639 804 345) is for education and entertainment purposes only. It is not intended as a substitute for professional financial, legal or tax advice. While we do our best to provide accurate information on the podcast, we accept no responsibility for any inaccuracies that may be communicated.

Flux does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) and ASIC RG 36.66. Flux Technologies Pty Ltd provides general advice on credit products under our own Australian Credit Licence No. 530103. The product information presented does not constitute an offer and we are not recommending or suggesting any particular product.

This document does not contain and should not be taken as containing any financial product advice or financial product recommendations. This document does not take into consideration any recipient’s objectives, financial situation or needs. Before making any decision relating to a

Schroders fund, you should obtain and read a copy of the product disclosure statement available at www.schroders.com.au or other relevant disclosure document for that fund and consider the appropriateness of the fund to your objectives, financial situation and needs. You should also refer to the target market determination for the fund at www.schroders.com.au. All investments carry risk, and the repayment of capital and performance in any of the funds named in this document are not guaranteed by Schroders or any company in the Schroders Group.

The material contained in this document is not intended to provide, and should not be relied on for accounting, legal or tax advice. Schroders does not give any warranty as to the accuracy, reliability or completeness of information which is contained in this document. To the maximum extent permitted by law, Schroders, every company in the Schroders plc group, and their respective directors, officers, employees, consultants and agents exclude all liability (however arising) for any direct or indirect loss or damage that may be suffered by the recipient or any other person in connection with this document.

Opinions, estimates and projections contained in this document reflect the opinions of the authors as at the date of this document and are subject to change without notice. “Forward-looking” information, such as forecasts or projections, are not guarantees of any future performance and there is no assurance that any forecast or projection will be realised. Past performance is not a reliable indicator of future performance. All references to securities,

sectors, regions and/or countries are made for illustrative purposes only and are not to be construed as recommendations to buy, sell or hold

Sign up for Flux and join 100,000 members of the Flux family