Learn how debt recycling can be used as a strategy to turn non-deductible debt, into tax-deductible debt.

You know the saying “work smarter not harder”? Well the same principle applies to your money. Being strategic about how you save, invest and pay down debt could be the difference that helps you reach your financial goals 10 or even 20 years sooner (than your coworkers) 😉

With recent interest rate cuts (and more predicted to follow), now is the perfect time to consider how to optimise your financial strategy… so that your money works harder for you, not the other way around.

If you have an owner-occupied mortgage, this debt is technically considered ‘good debt’. That’s because property has historically appreciated in value over time and you’re building equity in your home. But because this is your primary place of residence (PPOR), the interest you pay on this loan is not tax deductible.

One way to turn your non-deductible mortgage into a tax-deductible loan is through a strategy called ✨debt recycling✨

Essentially, you can pay down your home loan, then reborrow that same amount to invest.

Whether interest is tax-deductible depends on what the borrowed money is used for.

Interest on your home loan isn’t tax-deductible. But if you borrow to invest in income-generating assets (like shares or property), that interest can be tax-deductible. Same total debt - but more of it is working in your favour.

Meet Rachel:

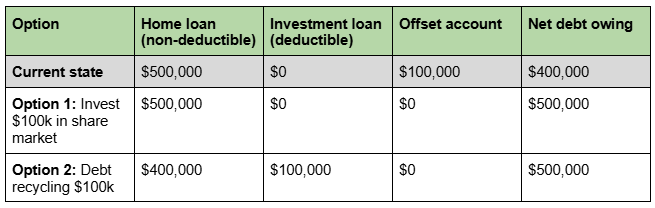

Rachel wants to start investing for her future.

She has two main options for investing:

Rachel hasn’t taken on extra debt - she’s just shifted the loan structure and put that money into investments.

If she’d taken the $100,000 from her offset and invested it directly, the interest on her original home loan would still be non-deductible.

But by paying it onto the loan first, then borrowing it again for investment, she’s changed the purpose of that $100,000 - this is what makes the interest potentially deductible.

Additionally, she could use any dividends from her investments to make additional repayments on her home loan to pay down this debt faster.

Debt recycling can be really risky stuff because you’re essentially using your home as a security for your investment. Additionally:

🚫 Dividends and capital growth on your investment is not guaranteed, and you’ll still need to make repayments on your loan even if your investment isn’t performing well

🚫 On a variable interest home loan your repayments could increase, which might put extra strain on your cashflow

🚫 This strategy only works if you actually use your dividends on paying down your non-deductible debt, so you’ll need to be disciplined.

Debt recycling can be a clever strategy to build wealth over time, but it needs to be done properly. If you're curious, it’s worth speaking to a mortgage broker and financial adviser to get it structured right.

Disclaimer: All information contained in the Flux app, www.flux.finance, www.joinflux.com, app.flux.finance and any podcast of Flux Media Pty Ltd (ABN 27 639 804 345) is for education and entertainment purposes only. It is not intended as a substitute for professional financial, legal or tax advice. While we do our best to provide accurate information on the podcast, we accept no responsibility for any inaccuracies that may be communicated.

Flux does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) and ASIC RG 36.66. Flux Technologies Pty Ltd provides general advice on credit products under our own Australian Credit Licence No. 530103.

Sign up for Flux and join 100,000 members of the Flux family